Restructuring of Industries to Take Place Fast

There are predictions that global oversupply of LCD display panels will continue until 2018. It seems that panel manufacturers will speed up process of industrial restructuring by changing produced items mainly to large products with high added values and changing operation rate.

Market research company called HIS Technology held ‘Korea Display Conference 2016’ Seminar at L-Tower in Yangjae-dong on the 22nd and presented such predictions. Because trend of global economy is proportional to growth of display industry, it is predicted that display industry will recover again after 2017 when global economy is expected to recover. Because China is making an aggressive facility investment, oversupply will continue until 2018.

“Profit ratio of manufacturers has become significantly worse as prices of LCD panels collapsed starting from second half of last year and profit ratio of first quarter of this year is also a lot lower than expectations.” said Director Jung Yun-sung of IHS Technology Korea. “We are at a situation where we have to restructure LCD industry no matter what such as modifying operation rate and price.”

According to analysis done by IHS, prices of LCD panels during second half of last year fell to later-end of 20% and middle end of 30% throughout major sizes such as 32-inch, 40-inch, 42-inch, 49-inch, 55-inch and others. Because percent margin of panel manufacturers also fell, AUO, Innolux, and Sharp recorded negative profit ratio in fourth quarter of last year. Samsung Display and LG Display only made front end of one digit profit.

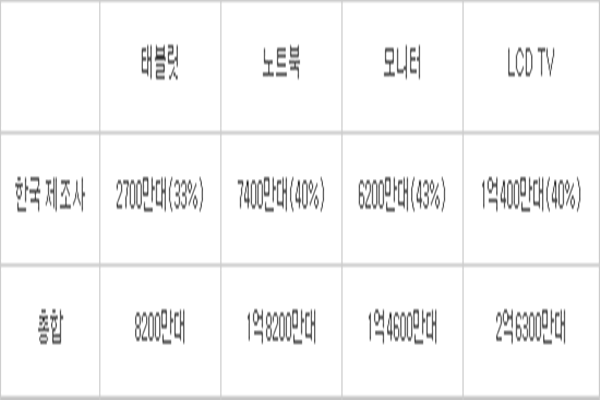

It seems that shipment of LCD TV panels will decrease from 274 million sheets from last year to 257 million sheets this year. TV sets will maintain last year’s shipment at 224 million and have 15% difference in supply and demand. Difference from last year was 22% and it was the greatest value since 2008.

IHS is predicting that a problem of oversupply will happen again this year due to stocks of LCD panels that occurred last year. Due to this problem, Chinese manufacturers along with South Korean and Taiwanese manufacturers are decreasing supply of 32-inch and are trying to maximize their profits by producing mostly large panels with 40-inch or above.

“South Korean panel manufacturers will compete with quality rather than quantity in LCD business now.” said Director Jung Yun-sung. “They are going to focus their capabilities in strengths that they already had such as large panels, 4K panels and others and focus on reducing production cost.”

As panel manufacturers are shifting their gears towards large panels, speed of converting to larger panels in display industry is going to be fast.

“Although average size of display was 39.3 inch last year, it is going to be 40 inch or above for the first time at 40.9 inch.” said President Park Jin-han of IHS Technology. “As there are more investments for 8th generation, prices of 40-inch or above panels will quickly decrease and there will be more amount of supply.”

This year is also a year when shipment of 55-inch UHD Panels surpasses shipment of Full HD Panels. It was important that difference in prices of 55-inch UHD and Full HD Panels quickly decreased. Although price of UHD Panel was 155% of price of Full HD Panel in 2013, IHS is predicting that Full HD Panels will quickly disappear in markets as difference became only 14% at the end of last year.

“This year and next year are the times when investments are focused on display industries.” said President Park Jin-han. “Because especially many LTPS (Low-Temperature Poly-Silicon) Panels are going to be used for LCD and OLED 176, it will be opportunistic for businesses that invest in LTPS.”

Staff Reporter Bae, Okjin | withok@etnews.com